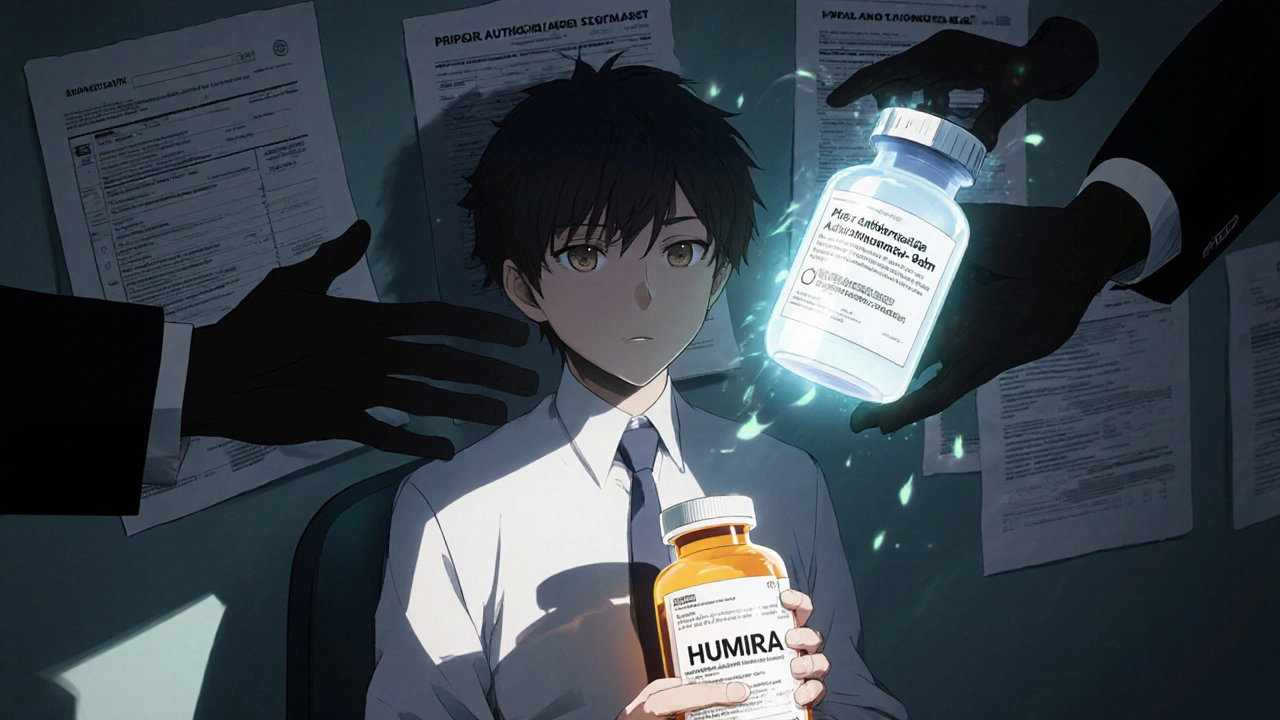

When you’re prescribed a biologic drug like Humira for rheumatoid arthritis or Crohn’s disease, you might expect your insurance to help lower the cost. But if your doctor suggests switching to a biosimilar - a cheaper, FDA-approved version of the same drug - you could hit a wall. Not because it’s less effective. Not because it’s unsafe. But because your insurance plan makes it harder to get.

Why Biosimilars Are Different From Generics

Biosimilars aren’t like generic pills. You can’t just swap one for the other like you would with brand-name aspirin and its generic version. Biosimilars are made from living cells - not chemicals - so they’re complex molecules that mimic, but don’t perfectly copy, their reference biologics. The FDA requires them to prove they work the same way, with no meaningful difference in safety or effectiveness. The first one, Zarxio, got approved in 2015. Since then, over 70 have been approved, and about 40 are actually on the market.That’s a lot of options. But here’s the problem: even though biosimilars cost 10% to 33% less than the original biologics, most insurance plans treat them the same way as the brand-name drugs. That means you’re still paying hundreds, sometimes over a thousand dollars a month out of pocket - even if you’re on the cheaper version.

Prior Authorization: The Bureaucratic Gatekeeper

Nearly every insurance plan that covers biologics requires prior authorization before you can get them. That’s a form your doctor has to fill out, explaining why you need the drug, what other treatments you’ve tried, and why this one is necessary. For Humira, it’s almost universal - 98.5% of plans require it.But here’s the twist: those same plans don’t make it easier for biosimilars. They apply the exact same strict rules. Your doctor has to jump through the same hoops whether you’re asking for Humira or its biosimilar. No shortcuts. No less paperwork. No faster approval.

That delays treatment. A 2024 survey found rheumatologists spend 3 to 5 hours a week just dealing with prior auth requests. One patient with severe arthritis waited 28 days to get started because the plan forced a trial of the biosimilar first - even though her condition was worsening. That’s not just inconvenient. It’s dangerous.

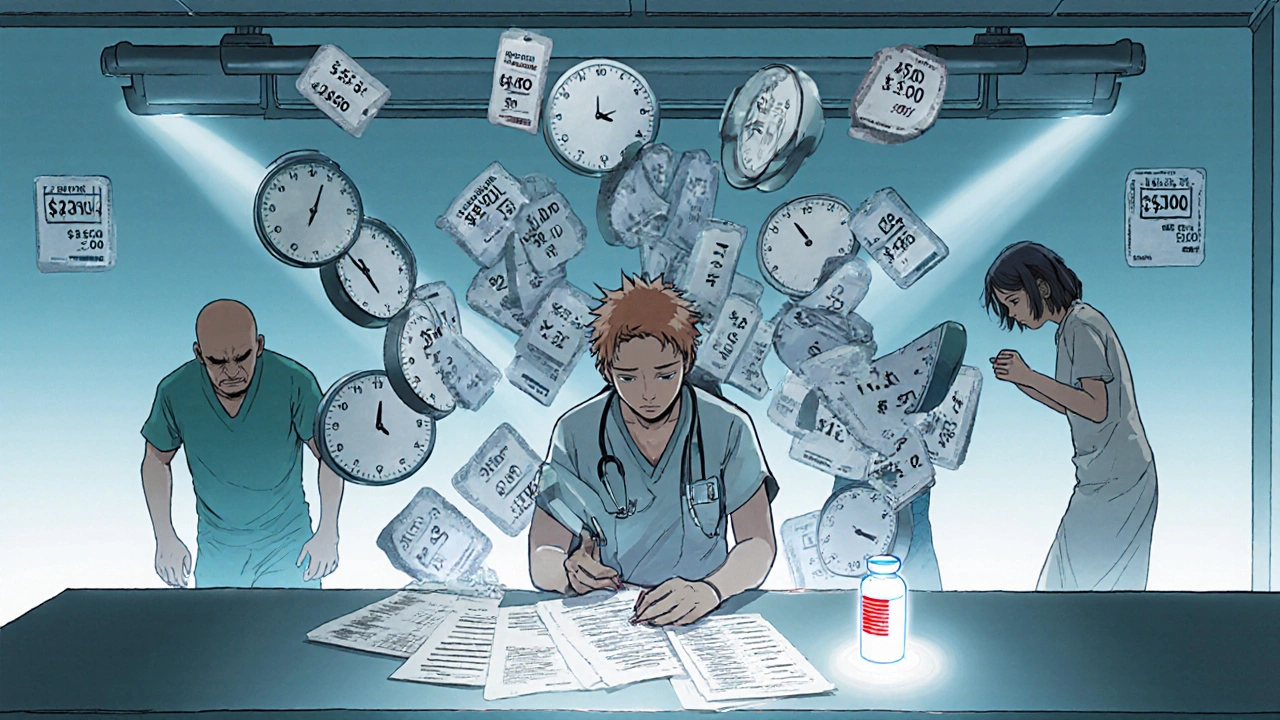

Tier Placement: The Hidden Cost Trap

Insurance plans organize drugs into tiers. Lower tiers mean lower costs. Tier 1 is usually generic pills. Tier 4 or 5? That’s where expensive biologics land. Most biosimilars are placed on the same high-cost tier as their brand-name counterparts. In fact, 99% of Medicare Part D plans put Humira and its biosimilars on the same tier in 2025.That’s a big deal. If you’re on a 33% coinsurance plan, and Humira costs $5,000 a month, you pay $1,650. The biosimilar might cost $4,200 - so you pay $1,386. That’s a $264 difference. For most people, that’s not enough to make switching worth the hassle. Especially when your doctor has to fight insurance for every step.

Only 1.5% of plans put biosimilars on a lower tier. That’s not a mistake. It’s a strategy. PBMs - the middlemen that manage drug benefits for insurers - are paid based on the list price of drugs. If a biosimilar is cheaper, they make less profit. So they keep them on the same tier, or even make them harder to access.

Why Insurers Resist Change

You might think insurers would jump at the chance to save money. And they do - on paper. The Congressional Budget Office estimates biosimilars could save the U.S. healthcare system $54 billion over the next decade. But in practice, the system is designed to protect the status quo.Big drugmakers like AbbVie, the maker of Humira, have spent years building contracts with PBMs that pay them rebates if they keep Humira on formularies. PBMs, in turn, use those rebates to lower premiums for insurers - but not for patients. So the savings never reach you. Meanwhile, biosimilars don’t offer the same kickbacks. That’s why, even though eight biosimilars for Humira are available, only half of Medicare Part D plans cover any of them.

Some PBMs are starting to flip the script. Express Scripts, OptumRx, and CVS Caremark now exclude Humira from their standard formularies entirely. That means if you want Humira, you have to appeal - and you’ll likely get the biosimilar instead. It’s not altruism. It’s economics. They’re forcing the switch by removing the expensive option.

What’s Changing in 2025

The tide is turning - slowly. In 2024, Medicare started requiring plans to report how they cover biosimilars. The results? 78% of plans now include at least one biosimilar alongside the brand-name drug. That’s progress. But coverage doesn’t mean access.The Office of Inspector General found that most plans still don’t give biosimilars a financial advantage. In response, CMS is now monitoring tier placement more closely. The Inflation Reduction Act gives them new tools to penalize plans that discriminate against biosimilars. If they enforce it, we could see a real shift.

Some insurers are already ahead of the curve. UnitedHealthcare and Cigna still don’t cover insulin biosimilars - even though eight are approved. But Express Scripts now places multiple Humira biosimilars on Tier 3 - the preferred specialty tier - with 25% coinsurance instead of 33%. That’s a real incentive. Patients pay less. PBMs still make money. Everyone wins - except the original drugmaker.

What This Means for You

If you’re on a biologic right now, here’s what to do:- Ask your doctor if a biosimilar is an option. Don’t assume it’s not covered.

- Check your plan’s formulary. Look up both the brand name and the biosimilar by its full name (like adalimumab-adbm for Cyltezo).

- If you’re denied, file an appeal. You have the right. Many denials get overturned.

- Ask if your plan has a step therapy requirement. If so, push back - especially if your condition is unstable.

- Use patient assistance programs. Many biosimilar makers offer co-pay cards that can cut your monthly cost to under $100.

Don’t let insurance rules stop you from getting the best, most affordable treatment. Biosimilars work. They’re safe. And they’re here. The system just hasn’t caught up yet.

Why This Matters Beyond Your Wallet

This isn’t just about money. It’s about access. Biologics treat chronic, life-altering conditions - autoimmune diseases, cancer, severe asthma. If patients can’t afford them, they skip doses. They delay treatment. Their conditions worsen. Hospital visits go up. Costs rise for everyone.Europe got this right. There, biosimilars make up over 80% of the market for drugs like Humira. Why? Because their health systems actively encourage switching. Lower tiers. Fewer barriers. Faster approvals.

The U.S. is behind. But it’s not too late. With better rules, better enforcement, and more pressure from patients and providers, we can fix this. The science is there. The savings are real. What’s missing is the will.

Asha Jijen

November 28, 2025 AT 10:22 AMWhy even bother with insurance when they just make you suffer? Biosimilars work, but they make it hard on purpose. So much for saving money.

Jonah Thunderbolt

November 29, 2025 AT 12:42 PMOh wow. 😱 So PBMs are literally choosing profit over people? And we call this a healthcare system? 🤡 I mean, come on. The fact that we’re still fighting this in 2025? I’m not even mad. I’m just disappointed. Like, deeply. 💔

Rebecca Price

November 29, 2025 AT 23:38 PMLet’s be real - this isn’t about cost. It’s about power. The system is rigged to protect legacy pharmaceutical revenue, not patient outcomes. And the worst part? Patients are being told to ‘just appeal’ like it’s that simple. 🤦♀️ You can’t appeal your way out of a broken system. We need structural reform, not Band-Aids. And yes - Europe’s model proves it’s possible. We’re just choosing not to be smart.

marie HUREL

November 30, 2025 AT 21:52 PMI’ve been on Humira for six years. Switched to a biosimilar last year after my doctor pushed. Took 47 days to get approved. My flare-up got worse. I cried in the pharmacy parking lot. But I did it. And now I pay $85 a month instead of $1,500. It’s not perfect. But it’s better. I wish more people knew this was possible. You just have to keep pushing.

Gayle Jenkins

December 2, 2025 AT 01:02 AMMy rheumatologist just told me last week that Express Scripts now puts three biosimilars on Tier 3. That’s huge. I didn’t believe it until I saw the formulary. My coinsurance dropped from 33% to 25%. That’s $150 a month saved. And no prior auth drama anymore. This is what change looks like. It’s slow, but it’s happening. Keep fighting. They’re starting to blink.

laura lauraa

December 2, 2025 AT 12:51 PMIt’s not just the PBMs. It’s the entire moral collapse of American capitalism. We have commodified suffering. We have turned healthcare into a spreadsheet. And now we’re surprised that people die because they can’t afford to live? The real tragedy isn’t the lack of biosimilars - it’s the lack of conscience. We’ve lost our soul. And no amount of co-pay cards can fix that.

Frances Melendez

December 2, 2025 AT 17:57 PMPeople like you who just say ‘just appeal’ are part of the problem. You don’t get it. Not everyone has the energy, time, or privilege to fight insurance bureaucracy. Some of us are working two jobs, raising kids, and still bleeding out from autoimmune flares. Your advice is toxic. Stop pretending it’s that easy.

reshmi mahi

December 3, 2025 AT 04:32 AMUSA still can’t figure out how to save money? 😂 India has biosimilars for 1/10th the price and no drama. We don’t need 78% coverage - we need 100% access. Why are we still playing this game? Your system is broken. Not the science. The greed.

Kaleigh Scroger

December 3, 2025 AT 09:42 AMLet me tell you what I’ve seen in clinic. Patients skip doses because they can’t afford the copay even on biosimilars. One woman with lupus stopped her meds for 9 months because her plan wouldn’t cover the co-pay card unless she used a specific pharmacy. She ended up in the ER with a kidney flare. That’s not healthcare. That’s negligence dressed up as policy. We need mandatory tier placement reform. No exceptions. No loopholes. And no more letting PBMs decide who lives and who doesn’t.

Gaurav Sharma

December 4, 2025 AT 09:36 AMEurope: 80% biosimilar adoption. USA: 1.5% lower tiers. The difference? Culture. You Americans love your brands. You worship logos. You’d rather pay $1,500 for Humira than take a ‘generic’ even if it’s identical. This isn’t about insurance. It’s about identity. You don’t want to be the person on the cheap drug. You want to be the person on the ‘real’ one. Sad.

Jebari Lewis

December 5, 2025 AT 01:15 AMI’m a nurse in a rural clinic. We have patients who drive 90 miles to get their biosimilar because their local pharmacy doesn’t stock it. They pay out of pocket because insurance won’t cover it. One guy told me, ‘I’d rather eat less so I can stay alive.’ That’s not a statistic. That’s a human being. We need to stop talking about ‘formularies’ and start talking about dignity. The science is there. The will? That’s what’s missing.

Elizabeth Choi

December 6, 2025 AT 16:51 PMLet’s not romanticize biosimilars. They’re not magic. Some patients have immune reactions. Some don’t respond as well. The data is promising, but it’s not universal. And yes, PBMs are greedy - but insurers are also trying to manage risk. The system is messy because biology is messy. Simplifying it to ‘greed vs. patients’ ignores the clinical complexity. We need nuance, not outrage.