Most people think their therapy copay is the full cost of treatment. You show up, hand over your insurance card, pay $30, and walk out. Easy. But that $30 is just one piece of a much bigger financial puzzle. If you’re in therapy for more than a few weeks, you could end up paying thousands more than you expected - and no one warns you about it. The real cost of therapy includes your deductible, coinsurance, out-of-pocket maximum, session frequency, and whether your therapist is in-network. Ignoring any of these means you’re flying blind.

What Your Copay Really Means

Your copay is the fixed amount you pay per session after you’ve met your deductible. But if you haven’t met your deductible yet, you’re not paying the copay at all. You’re paying the full session rate. That’s where people get tripped up.For example, let’s say your therapist charges $143 per session (the national average in 2024), and your insurance plan has a $1,500 deductible. If you start therapy in January and see your therapist every week, you’ll pay $143 each time until you’ve spent $1,500 out of pocket. That’s 10 to 11 sessions before your copay even kicks in. By then, you’ve already paid more than $1,400 - and you’re only halfway through a typical 12- to 16-session course of treatment.

Many patients don’t realize this until they get their first bill. Nearly 40% of people report being shocked by their therapy costs after treatment begins. The copay on your insurance card doesn’t tell you the whole story. It only tells you what you’ll pay after you’ve already paid a lot.

Deductibles, Coinsurance, and Out-of-Pocket Maximums

Insurance plans use three main tools to split costs: deductibles, coinsurance, and out-of-pocket maximums. Understanding how they work together is the only way to predict your total cost.- Deductible: The amount you pay before insurance starts covering part of the cost. In 2024, the average individual deductible for mental health services was $1,500, but some plans go as high as $3,000 or more.

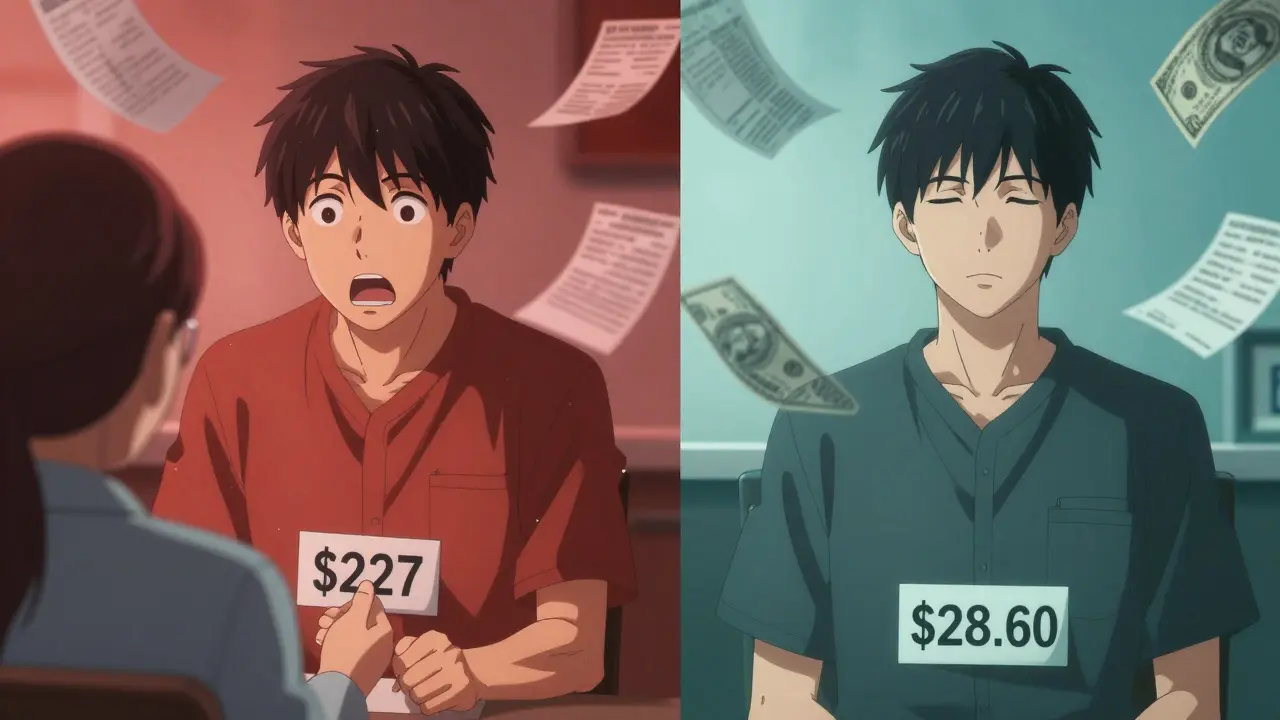

- Coinsurance: After you meet your deductible, you pay a percentage of the cost. Most plans use 20% to 40%. So if your session costs $143 and your coinsurance is 20%, you pay $28.60 - but only after hitting your deductible.

- Out-of-pocket maximum: The most you’ll pay in a year for covered services. In 2024, the federal limit for individual plans was $9,350. Once you hit that, insurance pays 100% of allowed costs for the rest of the year.

Here’s how it adds up: Imagine you need 20 sessions at $143 each ($2,860 total). Your deductible is $1,500, and your coinsurance is 20%. You pay full price for the first 10 sessions ($1,430). Then you pay $143 for the 11th session - hitting your $1,500 deductible. From session 12 onward, you pay 20% of $143 = $28.60 per session. For the remaining 9 sessions, that’s $257.40. Total out-of-pocket? $1,500 + $257.40 = $1,757.40. That’s a lot less than $2,860 - but still more than most people expect when they see their $30 copay.

In-Network vs. Out-of-Network: A Huge Difference

Choosing an in-network therapist can cut your costs in half. Out-of-network providers aren’t bound by your insurance company’s negotiated rates. That means they can charge whatever they want - and you might owe the difference.Let’s say you see an out-of-network therapist who charges $227 per session (the average in North Dakota). Your insurance only allows $143 as the “allowed amount.” You pay the full $227 upfront. Later, your insurer reimburses you 50% of the allowed amount ($71.50). So you’re out $155.50 per session - even if you’ve already met your deductible. That’s 5 times more than if you’d chosen an in-network provider.

Thriveworks’ 2024 data shows patients using out-of-network providers pay 40-50% more on average than those who stay in-network. And if you’re in a rural area or need a specialist, in-network options may be limited. That’s why it’s critical to ask your therapist: “Are you in-network with my plan?” before your first session.

What About Medicare and Medicaid?

If you’re on Medicare, the math changes. Medicare Part B covers 80% of therapy costs, so you pay 20%. For a $143 session, that’s $28.60 - but only if your therapist accepts Medicare assignment. If they don’t, you might pay more. And remember: you still have to meet your Part B deductible ($240 in 2024) before coverage starts.Medicaid, on the other hand, typically has no or very low copays. In many states, therapy is fully covered with no out-of-pocket cost. But eligibility varies by state, and not all therapists accept Medicaid. Always check with your provider.

Sliding Scale, Open Path, and Other Low-Cost Options

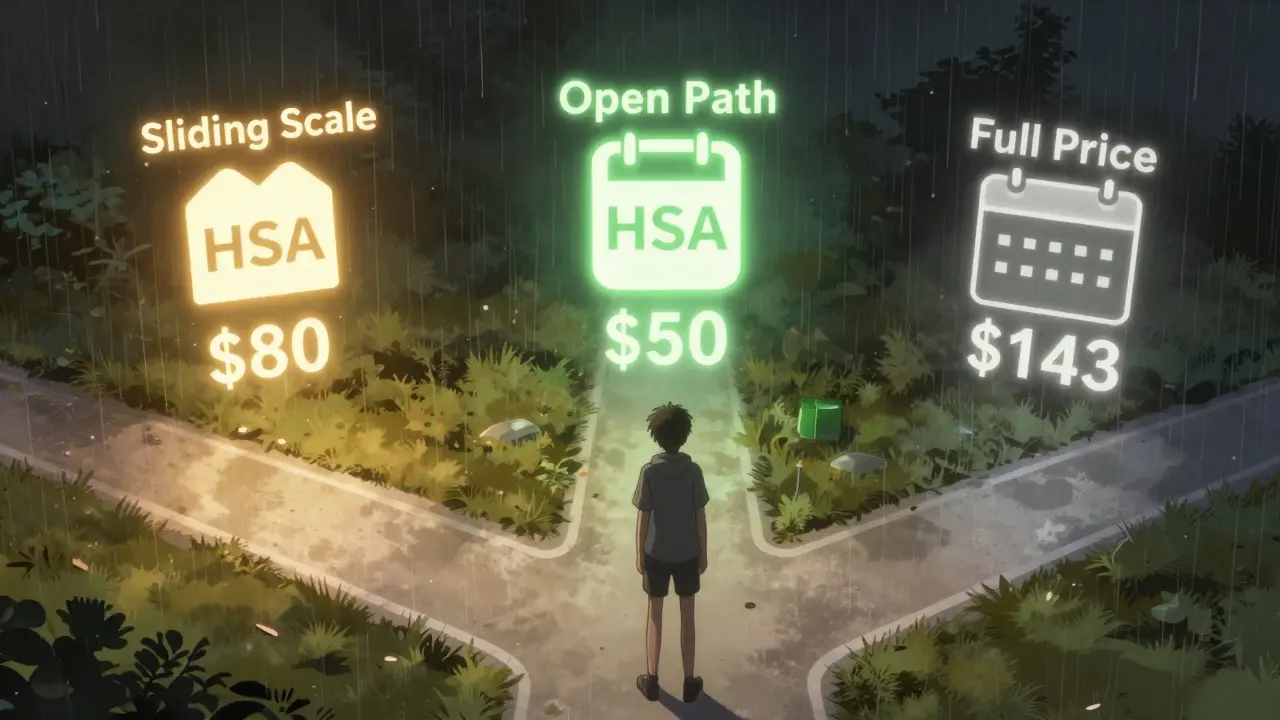

If you’re uninsured or have a high deductible, you don’t have to pay full price. About 42% of private practice therapists offer sliding scale fees based on income. That can cut costs by 30% to 50%. For example, if a session normally costs $143, you might pay $80 or less.Organizations like Open Path Collective connect people with therapists who charge $40 to $70 per session for uninsured or underinsured clients. University training clinics - where graduate students provide therapy under supervision - often charge 50-70% less than private practices. These aren’t second-rate options. They’re legitimate, licensed providers who are trained and supervised.

Don’t assume you can’t afford therapy if you don’t have great insurance. Ask. Many therapists want to help - and will adjust their rates if you ask.

How to Calculate Your Total Cost - Step by Step

Here’s a simple way to estimate your total therapy cost for the year:- Find your plan details: Log into your insurance portal or call customer service. Ask: What’s my deductible? My coinsurance? My out-of-pocket max? Do mental health and medical services share the same deductible?

- Know your therapist’s rate: Ask them how much they charge per session. Ask if they’re in-network. If not, ask what their “allowed amount” is with your insurer.

- Estimate sessions: Most people need 12-16 sessions for moderate anxiety or depression. For complex trauma, PTSD, or chronic depression, 20-30 sessions may be needed.

- Calculate Phase 1 (pre-deductible): Multiply your session cost by the number of sessions until you hit your deductible. Example: $143 x 10 = $1,430.

- Calculate Phase 2 (post-deductible): Multiply your copay or coinsurance by remaining sessions. Example: $28.60 x 10 = $286.

- Add it up: $1,430 + $286 = $1,716 total.

- Check the cap: Does this total exceed your out-of-pocket max? If yes, you’ll stop paying once you hit that limit.

Use tools like Alma’s free Cost Estimator or Rula’s calculator to plug in your numbers. They’ll show you exactly how much you’ll pay month by month.

Don’t Forget Hidden Costs

Therapy isn’t just the session fee. There are other expenses that add up:- Transportation: Gas, parking, or public transit to appointments.

- Time off work: Lost wages if you can’t take unpaid time.

- Medication: If you’re on antidepressants or anti-anxiety meds, those copays add up too. A $50 monthly prescription = $600 a year.

- Missed sessions: Many therapists charge full fees for no-shows. That’s another potential cost.

Shasta Health found that 30% of therapy-related stress comes from these hidden expenses, not the session fees themselves. Build them into your budget.

What to Do If You Can’t Afford It

If your total projected cost is too high, you have options:- Switch to a lower-cost provider (sliding scale, Open Path, training clinic).

- Reduce session frequency (biweekly instead of weekly).

- Time your therapy to align with your insurance year reset - start after January 1 if you’ve already met your deductible.

- Use your HSA or FSA account - you can pay for therapy with pre-tax dollars.

- Ask for a payment plan. Many therapists offer them.

Therapy is an investment - but it shouldn’t break you. The goal isn’t to pay the most. It’s to pay what you can afford, consistently, so you actually get better.

Is my copay the only thing I pay for therapy?

No. Your copay is only what you pay after meeting your deductible. Before that, you pay the full session rate. You may also pay coinsurance, which is a percentage of the cost, and you could owe money for out-of-network services or missed appointments.

How do I find out my deductible and coinsurance?

Log into your insurance company’s website or app and look for your “Summary of Benefits.” Call their customer service line and ask: “What’s my mental health deductible? What’s my coinsurance rate? Do medical and mental health services share the same deductible?” Write down the answers.

Can I use my HSA or FSA for therapy?

Yes. Therapy is a qualified medical expense under IRS rules. You can use pre-tax dollars from your Health Savings Account (HSA) or Flexible Spending Account (FSA) to pay for therapy sessions, copays, and even some online therapy platforms.

What if my therapist is out-of-network?

You’ll likely pay more. You’ll pay the full session fee upfront, then submit a claim to your insurer. They’ll reimburse you based on their “allowed amount,” which is often less than what the therapist charges. You’re responsible for the difference. Always ask your therapist for a superbill - a detailed receipt - so you can file for reimbursement.

Are there free or low-cost therapy options?

Yes. Open Path Collective offers sessions for $40-$70. University training clinics often charge 50-70% less than private practices. Some nonprofits and community health centers offer sliding scale fees. About 42% of private therapists adjust their rates based on income - ask if you qualify.

Does Medicare cover therapy?

Yes. Medicare Part B covers 80% of therapy costs after you meet your annual deductible ($240 in 2024). You pay the remaining 20%. If you have a Medigap Plan G, it covers your 20% coinsurance and deductible. Without it, you’re responsible for those costs.

What’s the average cost of therapy per session in 2026?

The average cost of a therapy session in the U.S. in 2024 was $143.26 without insurance. Costs vary by region - $176 in New York, $227 in North Dakota. With insurance, your out-of-pocket cost depends on your plan, but typically ranges from $20 to $50 per session after meeting your deductible.

Can I change therapists if the cost is too high?

Absolutely. You’re not locked in. If the cost is overwhelming, switch to a lower-cost provider - sliding scale, in-network, or community clinic. Your mental health matters more than sticking with one provider. It’s okay to shop around.

Dylan Patrick

March 13, 2026 AT 09:31 AMJust paid $280 last month for 4 sessions. Thought I was covered. Turns out I hit my deductible in March. Now I’m paying 30% coinsurance. No one warned me. I’m just glad I didn’t quit.

Elsa Rodriguez

March 14, 2026 AT 17:42 PMMy therapist charged me $190 for a no-show because I was sick. I had a fever. I cried. She still invoiced me. This system is designed to punish people who need help the most.

tynece roberts

March 15, 2026 AT 13:37 PMso like… i just found out my hsa covers therapy?? like… i’ve been paying out of pocket for 6 months. i could’ve used my hsa card. i’m so mad at myself. also my therapist said she does sliding scale but i was too shy to ask. now i’m gonna text her. lowkey embarrassed.

Alex MC

March 16, 2026 AT 01:55 AMThanks for laying this out clearly. It’s easy to assume the copay is the whole story. I’ve seen too many people quit therapy because they got hit with a surprise bill. Knowledge is power here.

Amisha Patel

March 17, 2026 AT 10:42 AMI’m from India and therapy here is expensive too, but we don’t have insurance. We pay outright. Still, I’m glad someone is talking about this. It’s not just an American problem.

Hugh Breen

March 19, 2026 AT 06:05 AMOMG YES. I switched to Open Path last year. $50/session. My therapist is AMAZING. I went from crying in my car every Monday to actually sleeping. If you’re struggling, just ask. No shame. 💪❤️

Serena Petrie

March 20, 2026 AT 20:25 PMMy deductible was $3,000. I gave up after 5 sessions.

Buddy Nataatmadja

March 20, 2026 AT 23:15 PMAs someone who moved from Indonesia to the U.S., I had no idea how complex this system is. Back home, mental health care is either free or out-of-pocket. Here? It’s a maze. I had to call 7 insurance reps before I understood anything.

Stephanie Paluch

March 21, 2026 AT 21:06 PMI didn’t even know HSA could be used for therapy. I’ve been paying with credit card. Now I’m digging through old receipts to see if I can get reimbursed. Thank you for this. 🙏

Ali Hughey

March 22, 2026 AT 06:46 AMEVERYTHING you said is true… BUT DID YOU KNOW THE GOVERNMENT AND INSURANCE COMPANIES ARE IN A SECRET AGREEMENT TO HIDE THE TRUE COST OF THERAPY?? THEY WANT YOU BROKE AND DEPRESSED SO YOU’LL STAY QUIET AND KEEP PAYING!! I FOUND A WHISTLEBLOWER ON 4CHAN WHO SAID THE DEDUCTIBLE SYSTEM WAS DESIGNED BY PHARMA LOBBYISTS TO KEEP PEOPLE IN THERAPY FOREVER!! 😱💸

Aaron Leib

March 23, 2026 AT 08:51 AMYou’re not alone. Many therapists offer payment plans if you ask. Don’t be afraid to say, ‘I really need this, but I’m stretched thin.’ Most will work with you.

Kathy Leslie

March 23, 2026 AT 18:54 PMI’m so glad I found a training clinic. I pay $30/session. My therapist is a grad student, but she’s brilliant. I’ve learned more in 8 sessions than I did in 20 with my old private therapist. And no one charged me for a missed session. 🥹

mir yasir

March 24, 2026 AT 06:59 AMThe systemic inefficiencies in American mental healthcare are emblematic of broader neoliberal decay. One must interrogate the commodification of affective labor within the clinical-industrial complex. The copay is merely a symptom, not the pathology.

rakesh sabharwal

March 24, 2026 AT 15:10 PMYou’re all missing the point. The real issue is that people don’t take responsibility for their own mental health. Therapy isn’t a right-it’s a privilege. Stop expecting others to subsidize your emotional labor.